As your student heads to college, financial responsibility moves from theory to practice fast. One of the most impactful things you can do to set them up for long-term success is help them start building credit. A strong credit score affects their ability to rent an apartment, finance a car, qualify for loans, and even secure some cell phone plans. Getting started early gives them a real advantage.

Why Credit Scores Matter

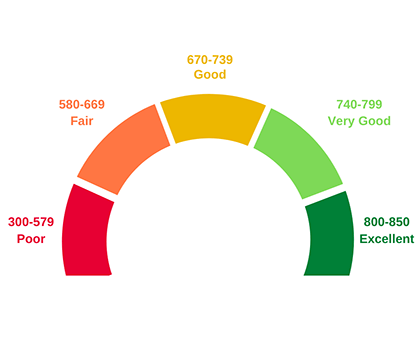

Lenders and landlords use credit scores to gauge how reliably someone manages money. A score of 700 or above generally signals responsible financial behavior and opens doors to better rates and terms. A low score, by contrast, can make borrowing more expensive and renting more difficult. The habits your student builds now will follow them into adulthood.

Four Ways to Help

Be a guide, not a rescuer. The goal is to teach financial responsibility, not to manage your student’s finances for them. Talk openly about the importance of paying bills on time and avoiding overspending. These conversations lay the groundwork for everything else.

Add them as an authorized user. One of the simplest ways to give your student a credit boost is to add them as an authorized user on one of your credit cards. Your positive payment history will be reflected on their credit report. A few things to keep in mind: your own responsible use of the card matters here, and you should have a clear conversation with your student about the ground rules before handing over the card.

Explore secured credit cards together. If adding them as an authorized user isn’t the right fit, a secured credit card is a solid alternative. With a secured card, your student deposits money into an account, which becomes their credit limit. A $300 deposit equals a $300 limit. They use the card for small purchases and pay the balance in full each month, building good habits with no risk of accumulating debt. After a year of responsible use, many secured cards convert to standard unsecured cards.

Talk through student loans and credit. If your student takes out loans, make sure they understand that loan accounts affect their credit score. Emphasize that making on-time payments after graduation is critical to their credit health. It is also worth explaining that private student loans typically appear on a credit report right away, while federal loans generally do not show up until repayment begins.

Building Credit Takes Time

Good credit is not built overnight. It takes consistent, disciplined behavior over months and years. By helping your student understand and engage with credit now, you are giving them more than a better number. You are helping them build a skill set that will serve them for a lifetime.

A fee-only financial planner can help your family think through how credit fits into a broader financial plan, whether that means college funding, student loan strategy, or laying the groundwork for your student’s financial independence after graduation.