Asset allocation — how you divide your investments among different asset classes like stocks, bonds, and cash — is the single most important driver of long-term investment performance and risk. Getting it right is more valuable than picking individual funds.

The Core Asset Classes

- Equities (Stocks): Historically the highest-returning asset class over long periods, but with significant short-term volatility. Suitable for money you won’t need for many years.

- Fixed Income (Bonds): Generally lower returns than stocks but with less volatility. Provide stability and income. Important ballast in portfolios for people approaching or in retirement.

- Cash and Cash Equivalents: Lowest risk and return. Important for emergency funds and short-term needs, but eroded by inflation over time if held excessively.

- Alternative Assets: Real estate, commodities, or other investments that may diversify portfolio risk.

Why Allocation Matters More Than Selection

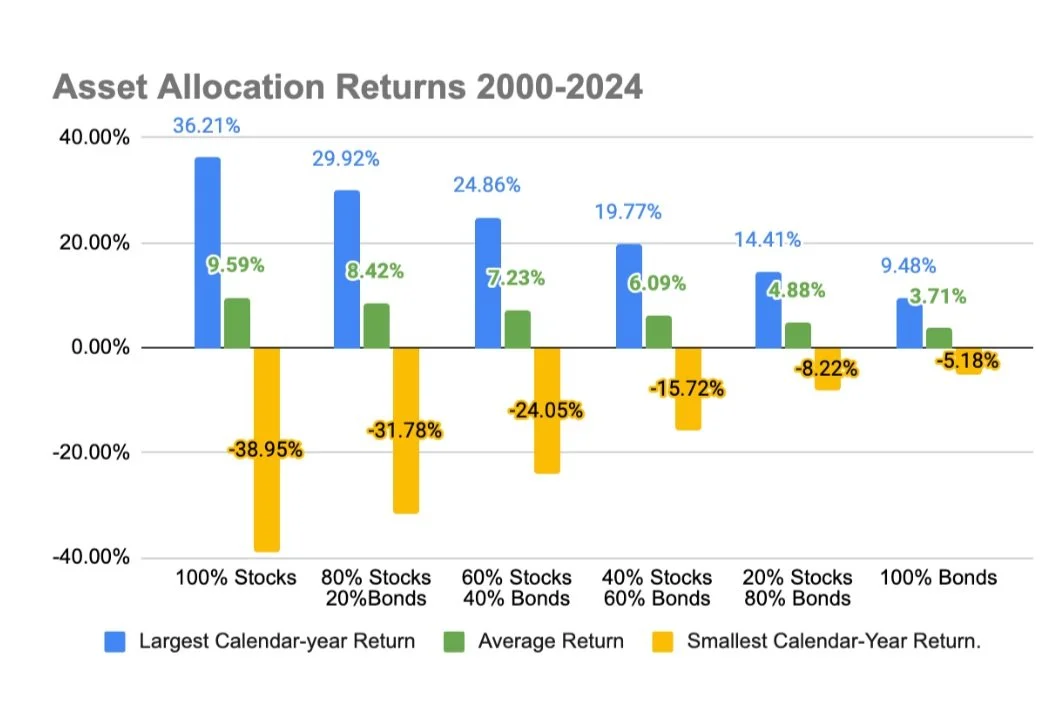

Academic research consistently shows that 80–90% of portfolio return variation is explained by asset allocation, not fund selection or market timing. A broadly diversified portfolio in the right allocation will typically outperform an active stock-picker over time.

How to Determine the Right Allocation

The right allocation depends on three factors:

- Time horizon: Longer timelines can absorb more volatility and warrant a higher equity allocation.

- Risk tolerance: How much drawdown can you emotionally and financially withstand without abandoning the plan?

- Income needs: If you’re drawing from the portfolio now (or soon), you need more stability to avoid selling equities at a loss during downturns.

Allocation Over Time

Most investors gradually shift from a growth-oriented allocation (more equities) to a more conservative allocation (more bonds and cash) as retirement approaches. This is sometimes called a “glide path.” Target-date funds do this automatically; individual portfolios need to be managed intentionally.

For families with a two-lifetime planning horizon — funding both a parent’s retirement and a child’s long-term care — asset allocation is more complex. Different portions of the portfolio may have very different time horizons and liquidity needs, requiring a segmented approach.