Your college student may have a full course load, a meal plan, and a dorm room — but if they leave school without a credit history, they’ll face real obstacles when they try to rent their first apartment, finance a car, or apply for a job with a background check. Starting smart beats starting over.

Why Credit Matters for College Students

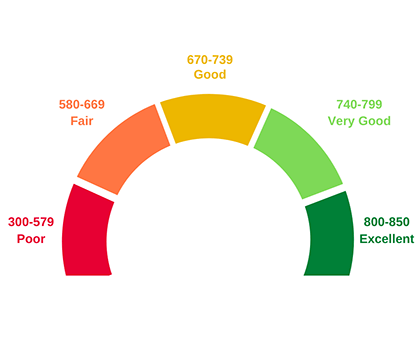

A credit score is essentially a financial report card that lenders, landlords, and even some employers use to assess reliability. It takes time to build, which is exactly why starting in college is such a strategic advantage.

The Best First Steps

- Become an authorized user: The simplest starting point. Add your student to one of your credit cards as an authorized user. Your positive payment history can flow to their credit file, giving them a head start without the risk of their own card.

- Secured credit card: Requires a cash deposit that becomes the credit limit. Easy to qualify for with no credit history and helps establish a payment track record.

- Student credit card: Designed for first-time cardholders with lower limits. Look for no annual fee and rewards on everyday spending categories.

Credit Score Fundamentals

The biggest factors in a FICO score are payment history (35%) and amounts owed (30%). Teach your student these two rules early:

- Pay the full balance every month. Carrying a balance and paying interest negates any benefit.

- Keep utilization below 30%. If the credit limit is $500, spending more than $150 per month before the statement closes can hurt the score even if the bill is paid on time.

What to Avoid

- Opening multiple new accounts at once (each application causes a small score dip)

- Missing even one payment — negative marks stay on a report for seven years

- Co-signing loans without full understanding of the obligation

For families with a child who has a disability, credit building must be balanced carefully against SSI resource limits. An authorized user arrangement typically does not create an asset in the student’s name. Consult a special needs planner before opening any account in a benefits recipient’s own name.